How to claim income tax refund on Lump-sum Withdrawal Payment for foreigners

Persons who do not have Japanese Nationality, when they lose their qualification as an insured person in the National Pension or Employee’s Pension and depart from Japan, can claim a Lump-sum Withdrawal Payment (Social Insurance) within two years from the date they no longer have an address in Japan.

The procedure to claim Lump-sum Withdrawal Payment is not complicated and you can apply yourself if you can prepare the following documents.

Document to be submitted

・Lump-sum Withdrawal Payment Claim Form

・Copy of your passport pages (verifying your name, date of birth, nationality, signature, and status of residence)

・Copy of your passport page (verifying your departure date from Japan)※

・Bank account information for the transfer of the Lump-sum Withdrawal payment

・National Pension Handbook and other documents verifying your Basic Pension Number

※If you submit your claim before your departure, please prepare 1) copy of resident card with registration of Moving-out Notification and the planned deletion date or 2) resident’s card exemption.

Income tax on Lump-sum Withdrawal Payment

For Lump-sum Withdrawal Payment for the National Pension, the income tax is not withheld at source.

However, for the Employees’ Pension, income tax at the rate of 20.42% is withheld at the time of payment. In other words, you will receive only about 80% of the amount of the Lump-Sum Payment.

In order to claim this withholding tax refund, you need to submit the “Tax Return for Refund Due to Taxation on Retirement Income at the Taxpayer’s Option” to the tax office.

By doing so, you will get a tax refund.

As soon as the Lump-sum Withdrawal Payment is remitted, the “Notice of Lump-sum Withdrawal Payment Determination” is sent to your home country.

Please send the original “Notice” to your Tax Agent. If your Tax Agent is a tax accountant, you can ask him or her to file your tax return and claim your refund immediately.

What is a Blue tax return system for income tax purposes in Japan?

Blue tax return system in Japan is intended to improve accounting practices of taxpayers and encourage honest self-assessment. Those who maintain proper accounts as required under the blue tax return system are given certain privileges for tax purposes. Basically, there are two types of income tax returns which taxpayers can choose from: White Form or Blue Form. Blue tax return is usually preferable because it offers some extra tax benefits, including special deductions.

Blue tax return system for individuals

When sole traders start a business in Japan, they can take advantage of income deduction by filing an application form for approval of filing blue return. White filing is the default, so if you do nothing you are automatically considered as a White-form filer. The tax authority requires the following for the blue return taxpayer:

1. Filing the application form by March 15.

2. Filing the application form within 2 months of business commencement if taxpayers start a business after January 16 of the year.

3. Taxpayers are required to keep correct accounting records and journals.

4. The blue tax return must be filed together with the balance sheet, income statement, and other documents indicating the items necessary for calculating the income amount.

What is the tax merits for blue tax return filing status?

Once a taxpayer obtains approval, he or she is entitled to file a blue return for all subsequent years. If the taxpayers meet the above requirements, the blue tax return system provides the following benefits:

1. A deduction of up to JPY650,000 is available if the taxpayers keep double-entry accounting records, and attach the income statement and the balance sheet on the return.

2. A deduction of up to JPY100,000 is available if the taxpayers keep single-entry records for their business.

3. A net loss for a year can be carried forward to the next 3 years.

4. A net loss for a year can be carried back to the preceding year.

5. The taxpayer is allowed to treat the payment of wages as deductible expenses when it is paid to relatives living in the same household (family employees).

Please note that JPY100,000 is deducted from the taxable income for property owners. If they operate more than 5 houses or a building with more than 10 rooms, JPY650,000 is deducted. If you plan to apply for JPY100,000 deduction, you need to prepare a spreadsheet which includes the detailed amount of revenue, expenses and cash balance. Using accounting software is recommended when you apply for JPY650,000 deduction.

Blue tax return system for corporations

If the company has blue-form tax return filing status, tax losses can be carried forward and utilized against taxable income for the following periods:

①9 succeeding years – tax losses incurred in fiscal years ending on or after April 1, 2008 and beginning before April 1, 2018

②10 succeeding years – tax losses incurred in fiscal years ending on or after April 1, 2018

Submission of an application should be done by whichever is earlier, either 3 months from the establishment of the company or the end of the first fiscal year. Generally, corporations file the application for blue tax return filing status together with a notification of commencement of business establishment to the tax office.

VAT on real estate transactions in Japan

Japanese consumption tax is sales based tax applied on supplies on certain goods and services within Japan, and it is similar to VAT/GST in AUS. The sale or lease of an asset located in Japan is a taxable transaction, however there are some transactions which are specifically excluded from being taxable, such as the sale or lease of land. The current consumption tax rate is 8%, and this will increase to 10% on 1 October 2019.

If you have an investment property in Japan, or use a property in running a business, there might be implications for income tax (including capital gains tax), consumption tax, and other related taxes. Japanese taxation can be difficult to handle especially for foreigners. Click here for more information about Japanese real estate taxation. The following will further explain Japanese consumption tax on real estate in Japan.

Buying a property in Japan

There is an increasing number of foreigners purchasing real estate here in Hakuba, Japan, ever since Hakuba became well-known for one of the greatest ski resorts in Asia. In the past, the most common investments are from Australia, but nowadays investments coming from Asia, such as China, Taiwan, Singapore are rapidly increasing.

The sale of land is excluded from being taxable for consumption tax purposes, however, when you buy a house or flat, or when build, it is subject to consumption tax.

For example:

Price of a house:JPY40,000,00

Consumption tax :JPY3,200,000 (JPY40,000,000×8%)

Commission to an agent:JPY1,200,000

Consumption tax: JPY96,000(JPY1,200,000×8%)

Rent out a property in Japan

Some of foreign investors acquire a property for investment purposes, and such non-resident owners consider leasing their properties. Also, non-Japanese living in Japan look for ski resorts as investment opportunities, or purchase properties as their second home. Such Japanese resident owners may consider leasing their properties during their absence as well.

When you rent out a property, the following transactions are non-taxable for cumsumption tax purposes:

-Leases of land

-Rental of housing (residential purpose)

If you rent out a property for residential purposes, you should not receive consumption tax from lessee. If you receive rental income from a rental cottage, flat, hotel, office tenant etc., it is subject to consumption tax.

In principle, consumption taxpayer status is determined depending on the amount of domestic taxable sales in the past. If your domestic taxable sales is over JPY10M a year, you are required to file a consumption tax return to the tax office. The amount of consumption tax payable is calculated based on the net of (i) consumption tax received on domestic taxable sales minus (ii) consumption tax suffered on domestic taxable purchase. There is a possibility that you will receive a consumption tax refund if the purchase price is high.

The taxable period is the respective fiscal year for a corporate taxable person, and the calendar year for an individual taxable person. If you need more information regarding your tax obligation in Japan, please feel free to contact us. If you need our tax advice before asking tax preparation services, we would be glad to offer an e-mail consultation.

Real estate tax guides and tips in Japan

If you have an investment property, build or renovate for profit, deal in land, or use a property in running a business, there might be implications for income tax (including capital gains tax), consumption tax, and other related taxes. In recent years, several foreigners have purchased properties in Japan, especially in Niseko or Hakuba, for both private and commercial purposes. They are surprised at the low prices of land and buildings compared to other international ski resorts. Japanese taxation can be difficult to handle especially for foreigners, and the following will further explain the real estate taxation in Japan.

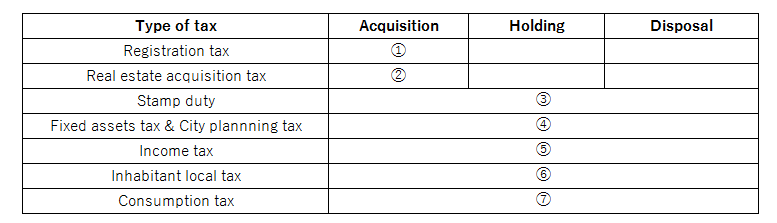

Below is an overview of real estate taxation in Japan based on each phase.

①Registration tax

When certain information is legally registered, it is subject to registration tax, such as registration of a Japanese company, registration of a branch of a foreign company, or registration of a change in the legal ownership of real estate.

“Registration” here refers to the recording of a legal interest in the official real estate registry (toukibo in Japanese) maintained at the local Legal Affairs Bureau.

Registration tax is calculated based on the value of the property, and the registration tax rate varies depending on the type of legal interest being registered.

Example:

Transfer of ownership by sale

・Land:1.5%*

・Building:2%

*Applicable for the period through 31 March 2019. This will be increased to 2% from 1 April 2019 onwards.

Establishment of a Japanese company or a branch

・KK(Kabushiki Kaisha):0.7% of stated capital (minimum JPY150,000)

・GK(Goudou Kaisha):0.7% of stated capital (minimum JPY60,000)

・Branch of a foreign company:JPY90,000

②Real estate acquisition tax

In Japan, real estate acquisition tax is payable by the purchaser every time land/buildings are transferred, regardless of whether or not the transfer is registered in the official real estate registry, and regardless of the amount of the purchase price, construction price, etc. The value of the property is used to calculate the amount of acquisition tax.

The basic tax rate is 4% of the appraised value of the property. Until March 31 2018, land and residential buildings are taxed at a special reduced rate of 3%. In addition to this, there are several tax benefits for real estate acquisition, when certain conditions are met.

You will receive a payment notice of real estate acquisition tax around 6 months after acquisition of properties. Please note that if you are an overseas resident, you are required to appoint a tax agent in Japan to pay tax.

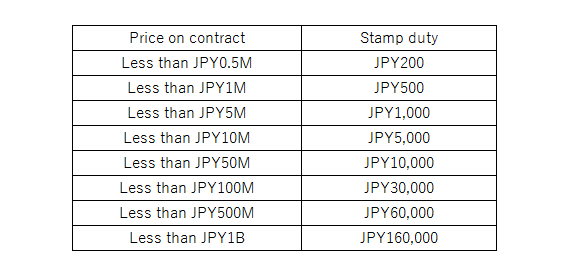

③Stamp duty

Stamp duty is payable on certain real estate documents, such as purchase and sale agreements for land/buildings, agreements to lease land/buildings, and construction contracts, etc. The levy is either based on the value involved or a flat rate.

Example:

The amount of stamp duty for real estate sale contracts (~31 March 2018)

④Fixed assets tax

Fixed assets tax is assessable on both real property and depreciable assets held at 1st January of each year. The tax is levied at 1.4% of the assessed value of real estate and depreciable assets. For lands used for residential purposes, there are certain tax benefits.

In addition, city planning tax is levied at a flat rate of 0.3% on the assessed value of real estate. City planning tax is levied together with the fixed assets tax.

You will receive a payment notice of fixed assets tax every year. Please note that if you are an overseas resident, you are required to appoint a tax agent in Japan to pay tax.

⑤Income tax ⑥Inhabitant local tax

Income tax is payable when you rent out a property even if you are an overseas resident. Also, capital gains are taxable when you sell a property.

Click for more information about income tax.

・Overview of Japanese taxation for individuals

・Guide to income tax refund in Japan

・Japanese tax on rental income

・Capital gains tax on real estate in Japan

⑦Consumption tax

Japanese consumption tax is sales based tax applied on supplies on certain goods and services within Japan, and it is similar to VAT/GST in AUS. The sale or lease of an asset located in Japan is a taxable transaction, however there are some transactions which are specifically excluded from being taxable, such as the sale or lease of land. The current consumption tax rate is 8%, and this will increase to 10% on 1st October 2019.

Guide to income tax refund in Japan

You might think that claiming an income tax refund in Japan can be confusing and complicated. Filing a tax return isn’t easy, and especially doing it in another country can be particularly challenging. K.S. Accounting has the expertise and vast experience in the international tax field in Japan, and we have the right people to handle your income tax needs. You can still claim your tax refund up to five years. Click here for more information about our taxation services.

Income tax refund for employees

If you work for a Japanese company and that’s your sole source of income in Japan, your company will take care of every tax matters for you. However, it would be advisable to file a tax return in a certain situation, as you can get a tax refund when certain conditions are met. For example, you can claim a tax refund in the following:

・If you left a company and your company didn’t carry out a year-end adjustment procedure for you, you may get a tax refund.

・If you have a large amount of medical expenses, you can apply for medical expenses deduction on your income tax return.

・Income tax on lump-sum withdrawal payments*

・If you buy or build your own home in Japan and has an outstanding loan balance, you can apply for special tax credit about the housing loan.**

*Certain persons who enrolled in Japanese public pension schemes for 6 months or longer can apply for lump-sum withdrawal payments to the Japan Pension Service after they leave Japan. When you receive the payments, income tax at a rate of 20.42% on the amount to be paid is withheld from the payment. In this case, you may claim a tax refund if you opt to file a tax return.

**There are a bunch of rules associated with this system. For example, the tax credit is only available for personal residences and cannot be applied for holiday homes, second homes or rental properties. The tax office will require a proof of residence. Your personal annual income must not exceed JPY30M, and the tax credit is only available for a period of 10 years from purchase. Please note that non-residents (those who are living overseas and who do not have residence in Japan) are eligible for purchase after April 2016.

Income tax refund for non-resident property owners

If the tenant of your property is a company (e.g. a company renting the apartment for their employees), the tenant must withhold 20.42% of the monthly rent. If the withholding tax paid is higher than your income tax payable, the excess can be refunded.

You must pay income tax on the profit you make from renting out the property, after deductions for “allowable expenses”. Allowable expenses are things you need to spend money on the day-to-day running of the property. If your property business is in deficit, you don’t need to pay tax and you can claim a tax refund. (Maintenance costs or depreciation expenses tend to be large for property business, and income tax can be often refunded.)

In that case, you will need to appoint a tax agent in Japan to file a tax return on your behalf to the tax office. We’d be glad to offer tax preparation services online even for overseas residents. If you have any concerns about Japanese taxation, please feel free to contact us.